"Four improvised areas of the City soon see long-term investment and job creation after being designated as “Qualified Opportunity Zones” under the federal Tax Cuts and Jobs Act of 2017, according to a release from the City of Sarasota."

"The program helps to revitalize low-income communities by providing tax advantages for private individuals and corporations who invest in an Opportunity Zone Fund. It encourages the private sector to reinvest capital gains from other investments into businesses and start-ups located in these Qualified Opportunity Zones, according to the release."

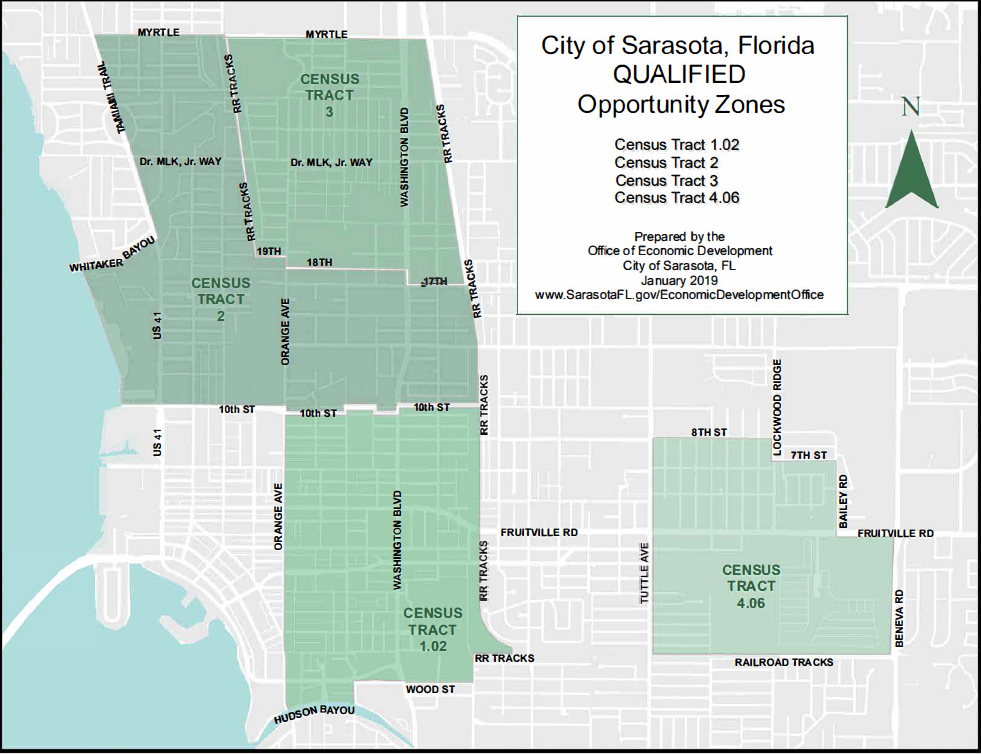

Poverty rates, family income, unemployment and other factors played a role in selecting the four zones in Sarasota.

Click to read the full article: http://www.mysuncoast.com/2019/02/15/four-areas-city-sarasota-named-opportunity-zones-investment-4/

For more information, visit SarasotaFL.gov or contact General Manager of Economic Development Steve Stancel at 941-316-8412.

Four areas of City of Sarasota designated ‘Opportunity Zones’ for investment

Revitalization encouraged under aegis of federal program

Four economically distressed areas of the city of Sarasota soon could see long-term investment and job creation after being designated “Qualified Opportunity Zones” under the federal Tax Cuts and Jobs Act of 2017, the city has announced.

The federal program “helps to revitalize low-income communities by providing tax advantages for private individuals and corporations” that invest in an Opportunity Zone Fund, a city news release explains. The program “encourages the private sector to reinvest capital gains from other investments into businesses and start-ups located in these Qualified Opportunity Zones,” the release adds.

Click to read the full article:

__________________________________________________________________________

The Federal Government enacted major new legislation to spur economic development. Opportunity Zones are designed to spur economic development by providing substantial tax benefits to investors.

______________________________________________

IRS Info

Q. What is an Opportunity Zone?

A. An Opportunity Zone is an economically-distressed community where new investments, under certain conditions, may be eligible for preferential tax treatment. Localities qualify as Opportunity Zones if they have been nominated for that designation by the state and that nomination has been certified by the Secretary of the U.S. Treasury via his delegation of authority to the Internal Revenue Service.

Q. How were Opportunity Zones created?

A. Opportunity Zones were added to the tax code by the Tax Cuts and Jobs Act on December 22, 2017.

Q. Have Opportunity Zones been around a long time?

A. No, they are new. The first set of Opportunity Zones, covering parts of 18 states, were designated on April 9, 2018. Opportunity Zones have now been designated covering parts of all 50 states, the District of Columbia and five U.S. territories.

Q. What is the purpose of Opportunity Zones?

A. Opportunity Zones are an economic development tool—that is, they are designed to spur economic development and job creation in distressed communities.

Q. How do Opportunity Zones spur economic development?

A. Opportunity Zones are designed to spur economic development by providing tax benefits to investors. First, investors can defer tax on any prior gains invested in a Qualified Opportunity Fund (QOF) until the earlier of the date on which the investment in a QOF is sold or exchanged, or December 31, 2026. If the QOF investment is held for longer than 5 years, there is a 10% exclusion of the deferred gain. If held for more than 7 years, the 10% becomes 15%. Second, if the investor holds the investment in the Opportunity Fund for at least ten years, the investor is eligible for an increase in basis of the QOF investment equal to its fair market value on the date that the QOF investment is sold or exchanged.

Q. What is a Qualified Opportunity Fund?

A. A Qualified Opportunity Fund is an investment vehicle that is set up as either a partnership or corporation for investing in eligible property that is located in a Qualified Opportunity Zone.

Q. Do I need to live in an Opportunity Zone to take advantage of the tax benefits?

A. No. You can get the tax benefits, even if you don’t live, work or have a business in an Opportunity Zone. All you need to do is invest a recognized gain in a Qualified Opportunity Fund and elect to defer the tax on that gain.

Q. I am interested in knowing where the Opportunity Zones are located. Is there a list of Opportunity Zones available?

A. Yes. The list of designated Qualified Opportunity Zones can be found at Opportunity Zones Resources and in the Federal Register at IRB Notice 2018-48. Further a visual map of the census tracts designated as Qualified Opportunity Zones may also be found at Opportunity Zones Resources.

Q: What do the numbers mean on the Qualified Opportunity Zones list, Notice 2018-48?

A: The numbers are the population census tracts designated as Qualified Opportunity Zones.

Q: How can I find the census tract number for a specific address?

A: You can find 11-digit census tract numbers, also known as GEOIDs, using the U.S. Census Bureau’s Geocoder. After entering the street address, select ACS2015_Current in the Vintage drop-down menu and click Find. In the Census Tracts section, you’ll find the number after GEOID.

Q. I am interested in forming a Qualified Opportunity Fund. Is there a list of Opportunity Zones available in which the Fund can invest?

A. Yes. The list of designated Qualified Opportunity Zones in which a Fund may invest to meet its investment requirements can be found at Notice 2018-48.

Q. How does a corporation or partnership become certified as a Qualified Opportunity Fund?

A. To become a Qualified Opportunity Fund, an eligible corporation or partnership self-certifies by filing Form 8996, Qualified Opportunity Fund, with its federal income tax return. Early-release drafts of the form and instructions are posted, with final versions expected in December. The return with Form 8996 must be filed timely, taking extensions into account.

Q: Can a limited liability company (LLC) be an Opportunity Fund?

A: Yes. A LLC that chooses to be treated either as a partnership or corporation for federal tax purposes can organize as a Qualified Opportunity Fund.

Q. I sold some stock for a gain in 2018, and, during the 180-day period beginning on the date of the sale, I invested the amount of the gain in a Qualified Opportunity Fund. Can I defer paying tax on that gain?

A. Yes, you may elect to defer the tax on the amount of the gain invested in a Qualified Opportunity Fund. Therefore, if you only invest part of your gain in a Qualified Opportunity Fund(s), you can elect to defer tax on only the part of the gain which was invested.

Q. How do I elect to defer my gain on the 2018 sale of the stock?

A. You may make an election to defer the gain, in whole or in part, when filing your 2018 Federal Income Tax return. That is, you may make the election on the return on which the tax on that gain would be due if you do not defer it.

Q. I sold some stock on December 15, 2017, and, during the required 180-day period, I invested the amount of the gain in a Qualified Opportunity Fund. Can I elect to defer tax on that gain?

A. Yes. You make the election on your 2017 return. Attach Form 8949, reporting Information about the sale of your stock. Precise instructions on how to use that form to elect deferral of the gain will be forthcoming shortly.

Q. Can I still elect to defer tax on that gain if I have already filed my 2017 tax return?

A. Yes, but you will need to file an amended 2017 return, using Form 1040X and attaching Form 8949.

Q. How can I get more information about Opportunity Zones?

A. Over the next few months, the Treasury Department and the Internal Revenue Service will be providing further details, including additional legal guidance, on this new tax benefit. More information will be available at Treasury.gov and IRS.gov.